SECURE ACT 2.0 AND INHERITED IRAS: WHAT CHANGED AND WHAT YOU NEED TO DO NOW

You inherited your parent's IRA. It has $400,000 in it.

Under the old rules, you could have stretched distributions over 30+ years, keeping most of the money growing tax-deferred.

Under SECURE Act 2.0, that changed. You have 10 years to empty the account. Then the tax bill comes due.

For many beneficiaries, this means paying $120,000 to $160,000 in federal and California state taxes on that inheritance. Money that should have gone to your retirement is gone.

This isn't theoretical. SECURE Act 2.0 went into effect January 1, 2023. If you inherited an IRA after that date, this applies to you. If you're planning your estate and want to protect your children's inheritance, you need a different strategy.

Here's what changed, why it matters, and what to do about it.

Andrew Kern

Sonoma County Estate Planning, Trust Administration, and Probate Attorney

Jump to…

Get Help With IRA Inheritance Matters. Request Now

What is SECURE Act 2.0 and Why It Matters

The SECURE Act 2.0 (Setting Every Community Up for Retirement Enhancement Act) is federal legislation passed in December 2022. It made sweeping changes to retirement account rules, including inherited IRAs.

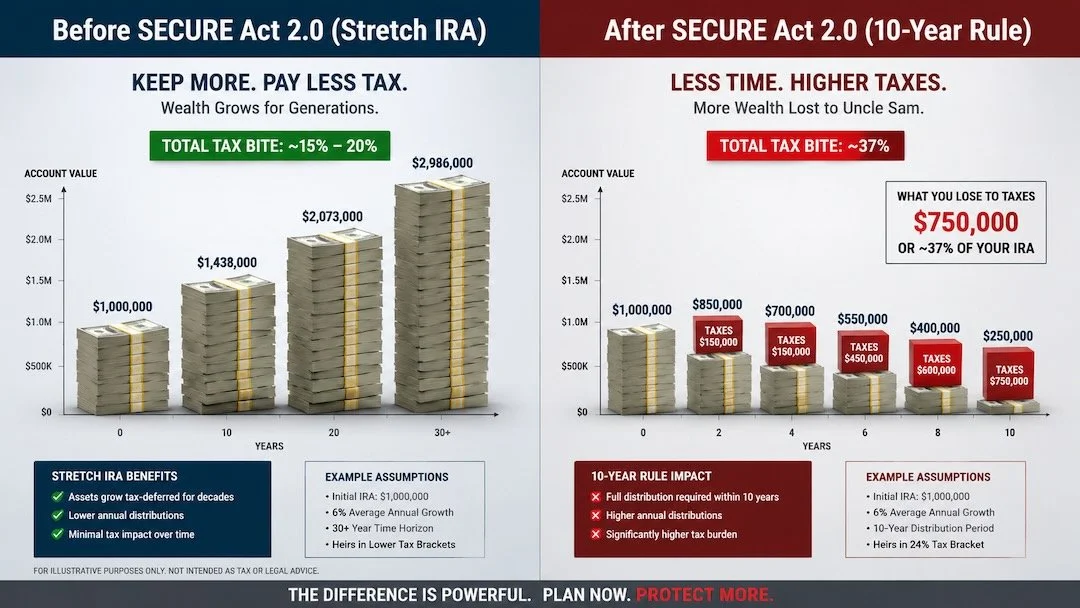

The most impactful change: the death of the "stretch IRA."

For decades, inheriting an IRA was considered a financial blessing. The beneficiary could stretch distributions over decades, keeping the account growing tax-deferred. A $500,000 inherited IRA could turn into $1 million or more by the time it was fully distributed.

SECURE Act 2.0 ended that. Congress wanted to increase immediate tax revenue. The solution: force beneficiaries to empty inherited IRAs faster.

The impact hits hardest in high-tax states like California, where state income tax on top of federal tax creates brutal consequences for beneficiaries.

If you inherited an IRA after January 1, 2023, or if you're planning your estate, you need to understand these rules. Most people don't. Most financial advisors aren't even explaining it clearly to clients.

The Old Rule: Stretch IRAs Were the Gold Standard

Before 2020, inherited IRA rules were beneficiary-friendly.

If you inherited an IRA from someone who wasn't your spouse, you could use the "Stretch IRA" strategy. You'd take only the required minimum distribution (RMD) each year based on your own life expectancy, which could be 30, 40, or even 50+ years.

Example: A 35-year-old inherits a $500,000 IRA. Under the old rules, they take distributions over roughly 50 years (their remaining life expectancy). The account keeps growing tax-deferred. By the time it's fully distributed, the balance could have grown to $1.5 million or more.

Taxes are paid annually on distributions, but small distributions mean small tax bills each year. The bulk of the money stays invested and compounds.

The Stretch IRA was one of the best wealth-transfer tools. Parents loved it. Financial planners marketed it. Beneficiaries benefited massively.

Then Congress changed the rules. Twice.

The New Rule: The 10-Year Window for Most Beneficiaries

SECURE Act 1.0 (passed in 2019, effective 2020) shortened the Stretch IRA. Most non-spouse beneficiaries could no longer stretch over their life expectancy. Instead, they had 10 years to empty the account.

But there was ambiguity: did they have to take annual distributions, or just empty it by year 10?

The IRS initially said just empty it by year 10. Beneficiaries could leave the money untouched for nine years, then withdraw it all in year 10.

SECURE Act 2.0 (passed December 2022, effective January 1, 2023) clarified this. The IRS released guidance in 2023 and 2024 that requires "annual distributions" starting in year 2 if you inherit after 2023. The amounts are still being debated, but the intent is clear: beneficiaries can't defer all distributions to year 10.

The effect: your inherited IRA gets distributed much faster, creating a massive tax bill concentrated over a short period..

Who Gets Hit Hardest by SECURE Act 2.0

Not everyone is equally affected. The damage depends on your situation.

Adult children inheriting large IRAs from parents. A 40-year-old inheriting $750,000 faces a brutal 10-year forced withdrawal schedule. If they're still working, this inheritance gets stacked on top of their salary, potentially pushing them into a higher tax bracket. In California, the marginal tax rate could be 40%+ (combined federal and state). They lose 40% of that inheritance to taxes.

High-income professionals in California. If you're a doctor, attorney, or business owner earning $200,000+ annually, inheriting a substantial IRA creates a tax nightmare. The additional IRA distributions push you into the top tax bracket. Every dollar of inherited IRA is taxed at your highest marginal rate.

Young beneficiaries. The younger you are, the worse SECURE Act 2.0 hits. A 25-year-old inheriting an IRA has 60+ years until retirement. They could have used the Stretch strategy to fund decades of retirement savings. Now they have 10 years. If they don't have the cash flow to absorb the distributions without touching the money, they're forced to spend it.

Beneficiaries in high-tax states. California's state income tax is brutal. A $300,000 inherited IRA creates roughly $120,000 in federal taxes plus $40,000+ in California state taxes. Total: $160,000 gone. The beneficiary keeps $140,000 of the original $300,000.

Multiple beneficiaries. If an IRA is split among three children, each gets a smaller inherited IRA—but each faces the same 10-year deadline. There's no spreading the tax burden across beneficiaries or time.

Exceptions: Who Can Still Stretch Their IRA

SECURE Act 2.0 isn't absolute. Specific categories of beneficiaries still get favorable treatment.

Spouses. If you inherit your spouse's IRA, you can treat it as your own. You can delay distributions until age 72, then take RMDs based on your life expectancy. This is the only true "Stretch IRA" path remaining. If you're a non-working spouse, this is incredibly valuable—you could stretch distributions 30+ years.

Disabled or chronically ill beneficiaries. If you have a disability (as defined by the IRS) or are chronically ill, you can still stretch the IRA over your life expectancy. This exception is critical for protecting inheritances for beneficiaries with special needs or long-term health conditions.

Minors. If the IRA is inherited by a minor child of the deceased, they get an exception. But it's limited: they can stretch only until they turn 30. Starting at age 30 (or when they reach legal age, whichever is later), they have 10 years to empty it.

Beneficiaries within 10 years of the deceased's age. If you're within 10 years of the deceased's age (younger or older), you can still use a life expectancy calculation. This exception is narrow but helps some adult children inherit from much older parents.

Certain trusts or estates. Some trust structures still get favorable treatment, but the rules are complex and getting more restrictive. Working with an attorney on this is essential.

Everyone else: the 10-year rule applies.

How Much Will Your Inherited IRA Actually Cost in Taxes

Let's do the math. This is where the pain becomes real.

Scenario 1: $400,000 Traditional IRA, 45-year-old beneficiary in California

Inherited amount: $400,000

10-year distribution schedule: roughly $40,000/year average

Beneficiary's other income: $120,000/year salary

Combined annual income during distribution years: $160,000/year

California + federal marginal tax rate: approximately 37% (32% federal + 5% California, varying slightly year to year)

Estimated taxes on distributions: roughly $148,000 total over 10 years

Actual money beneficiary keeps: $252,000

The remaining $148,000 went to taxes.

Scenario 2: $750,000 Roth IRA, 35-year-old beneficiary in California

Wait—if it's a Roth IRA, there are no income taxes on the distributions, right?

That's partially true. Roth IRA distributions themselves aren't taxable. But Roth IRAs are also subject to the 10-year rule, and the money is still forced out of the account. The tax impact is smaller but the loss of compounding is massive.

If that $750,000 Roth IRA had grown for another 30 years, it could have become $2+ million. Now it becomes roughly $750,000-$900,000 (depending on how it's invested during the 10 years). The beneficiary loses $1+ million in growth.

Tax Planning Strategies for California Beneficiaries

If you've inherited or will inherit an IRA, the damage isn't inevitable. Strategic planning can soften the blow.

Strategy 1: Distribute to a Roth conversion IRA (if applicable)

If you inherit a Traditional IRA, you can convert portions to a Roth IRA. You pay taxes on the conversion now, but future growth and distributions are tax-free.

This sounds counterintuitive: pay more taxes now to save taxes later. But if:

You expect to be in the same or higher tax bracket in 10 years

You have cash on hand to pay the conversion taxes

You want to leave tax-free money to your own beneficiaries

Then converting portions is smart. You're essentially accepting a smaller tax hit now (when it's spread over time) instead of a larger hit later (when distributions are concentrated).

Strategy 2: Accelerate distributions in low-income years

If you have a year with lower income (sabbatical, job loss, early retirement), take larger distributions from the inherited IRA that year. Your marginal tax rate is lower. You pay less tax on the distribution.

Strategy 3: Time your employment changes

If you're considering changing jobs, retiring early, or taking a sabbatical, coordinate it with inherited IRA distributions. Retire the year after inheriting—take distributions in low-income years, reduce taxes substantially.

Strategy 4: Use charitable giving strategically

If you're charitable, coordinate inherited IRA distributions with charitable giving. Donate distributions to charity rather than keeping the after-tax money. The tax-deduction can offset the distribution's tax cost.

Strategy 5: Work with a tax professional before the year you inherit

Don't wait until April 15 after your first inherited distribution. Talk to a tax attorney or CPA in Petaluma or Sonoma County immediately after inheriting. Plan the 10-year distribution strategy in advance. The right plan can save tens of thousands of dollars.

What to Do Right Now if You've Already Inherited an IRA

If you inherited an IRA after January 1, 2023, you're in the window. The 10-year clock is ticking.

Step 1: Identify what you inherited. Is it a Traditional IRA, Roth IRA, SEP IRA, or SIMPLE IRA? Different rules apply.

Step 2: Confirm the original owner's death date. This determines your deadline. If death was in 2023, your deadline is December 31, 2033. If death was in 2024, your deadline is December 31, 2034.

Step 3: Check if you qualify for an exception. Are you the spouse? Disabled? Chronically ill? A minor? Within 10 years of the deceased's age? If you qualify for an exception, your rules are different.

Step 4: Review the account value. Get the most recent statement. This determines your tax exposure.

Step 5: Create a distribution schedule. Don't leave this to chance. Work with a financial advisor and tax professional to map out distributions over the next 10 years. Include taxes in the calculation.

Step 6: Consider Roth conversions. If it's a Traditional IRA, evaluate whether converting portions to a Roth makes sense. This is math-dependent.

Step 7: Document everything. Keep records of all distributions, conversions, and taxes paid. The IRS will scrutinize inherited IRAs closely over the next decade.

How to Plan Your IRA for Your Beneficiaries in Petaluma and Sonoma County

If you're the IRA owner (not the beneficiary), SECURE Act 2.0 should change how you think about retirement accounts and estate planning.

Strategy 1: Maximize beneficiary-friendly assets while you're alive.

If you anticipate your beneficiaries will face painful inherited IRA taxes, spend down your IRA while you're alive. Distribute more money to yourself, pay the taxes now (at lower rates than your beneficiaries will pay), and pass non-IRA assets instead.

This sounds backwards—you want to keep your retirement money—but for high-income earners, it's smart. Your beneficiaries pay less total tax if you pay some of it before you die.

Strategy 2: Use Roth IRA conversions while you're alive.

Convert portions of your Traditional IRA to a Roth. Pay taxes on the conversion now. After five years, Roth IRA balances grow tax-free forever (for your beneficiaries and beyond). This is perhaps the single best tool to protect your beneficiaries from SECURE Act 2.0.

Strategy 3: Maximize Roth contributions annually.

If you're eligible, max out Roth IRA contributions ($7,500/year if 50+). Roth contributions grow tax-free and are inherited tax-free. It's not much, but over decades it compounds.

Strategy 4: Consider life insurance as an inheritance tool.

If IRAs aren't tax-efficient to inherit, consider life insurance instead. Leave life insurance proceeds to your beneficiaries rather than IRAs. Life insurance death benefits are income-tax-free. Your beneficiaries get the same money, but with no tax burden.

Strategy 5: Update your beneficiary designations.

Make sure your IRA beneficiary designations are current and intentional. Name specific people, not your estate. Beneficiary designation mistakes can compound SECURE Act 2.0's problems.

Step 6: Work with an estate planning attorney now.

SECURE Act 2.0 makes comprehensive estate planning essential. An attorney can review your overall situation and recommend the best strategy for your IRAs, other retirement accounts, and overall estate.

The Takeaway

SECURE Act 2.0 fundamentally changed inherited IRA rules. The Stretch IRA is gone for most beneficiaries. The 10-year window is real, and it's short.

If you've inherited an IRA, don't ignore it. The longer you wait to plan, the more constrained your options. If you own an IRA and want to protect your beneficiaries, start Roth conversions or other planning strategies now.

California's high state income tax makes this worse. A beneficiary in Petaluma or Santa Rosa pays significantly more tax on inherited distributions than someone in a low-tax state.

The good news: tax planning and strategic distributions can reduce the damage. You don't have to accept the full impact.

Call Law Office of Andrew Kern at (707) 658-4602 if you need help planning your estate around SECURE Act 2.0. We serve Petaluma, Santa Rosa, and all of Sonoma County. We can review your IRA situation and recommend strategies to protect your beneficiaries.

Don't leave your inheritance to chance. Plan now.